What is 3D Secure

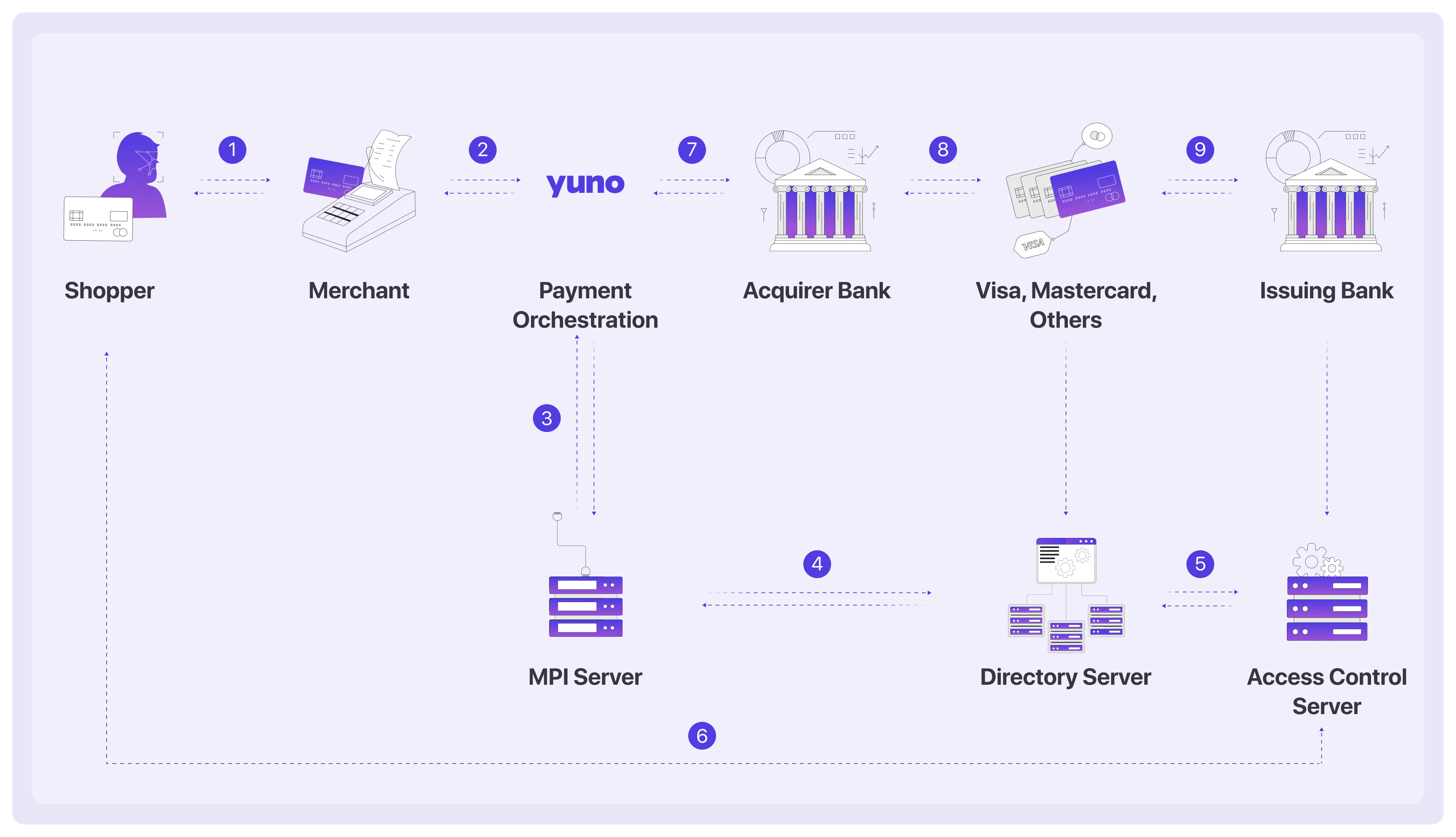

3D Secure (3DS) is a security protocol designed to prevent fraudulent use of credit cards in card-not-present (CNP) transactions. Introduced in 1999, it adds an extra verification step during online purchases to authenticate customers and reduce fraud risk. The flux below presents a payment process using 3DS:

Key components of 3DS

- Merchant Plugin Interface (MPI): Initiates the verification process and securely exchanges information between the merchant, scheme directory server, and issuing bank.

- Scheme Directory Server (DS): Acts as a centralized database that identifies the issuing bank and determines the authentication method.

- Issuer Access Control Server (ACS): Verifies the cardholder’s identity during a 3DS transaction. The ACS evaluates authentication requests and performs risk assessments based on the bank’s policies.

3D Secure 2 (3DS2)

Released in 2016, 3D Secure 2 (3DS2) enhances security while improving the user experience. Unlike the original 3DS, which relied on static passwords, 3DS2 introduces biometric authentication and token-based verification for a smoother, more secure process.Key improvements of 3DS2

- Supports authentication via biometrics, one-time passwords, and risk-based authentication.

- Reduces transaction friction with a seamless flow for trusted customers.

- Enhances fraud detection through detailed data sharing between merchants and banks.